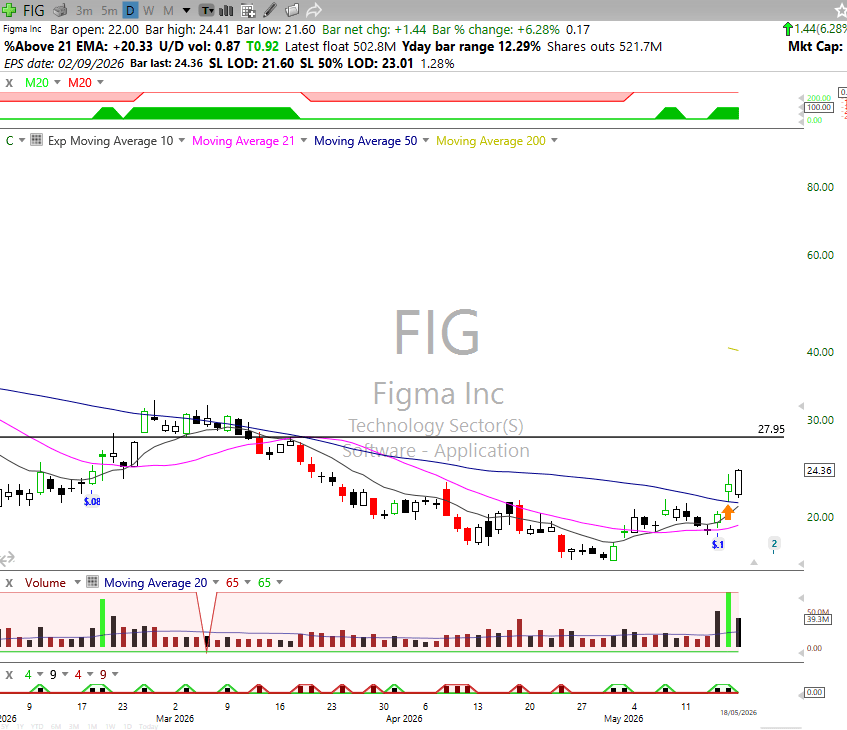

Entry price – 22.57

SL – 21.10

Risk – 1 dollar 47 cents

Time of entry – 14:57

Catalyst / setup – Ep 9 million

Earnings:

- 🟩 Earnings Growth YoY: EPS grew to $0.10 vs. $0.04 last year (+150%)

- 🟥 Earnings Growth QoQ: EPS declined from $0.18 in Q4 2025 to $0.10 in Q1 2026 (-44%)

- 🟩 Earnings Surprise vs. Estimates: $0.10 vs. $0.06 expected (+66.7% beat)

- 🟩 Sales Growth YoY: Revenue rose to $333.4M, up 46% YoY

- 🟩 Sales Growth QoQ: Revenue increased from $304M in Q4 2025 to $333.4M (+9.7% QoQ)

- 🟩 Sales Surprise vs. Estimates: $333.4M vs. $316.3M expected (+5.4% beat)

- 🟥 Margins YoY: Non-GAAP operating margin guidance for FY26 lowered to ~9% from ~12% in FY25 due to AI investments

- 🟩 Guidance Changes: Raised FY26 revenue guidance to $1.422B–$1.428B and raised operating income outlook

- 🟥 Short Ratio: Elevated bearish sentiment remains after the stock’s large post-IPO decline; short interest remains above average for software peers. ###

- 🟩 Fund Holdings % Change: Institutional ownership continues rising post-IPO as funds added exposure following multiple earnings beats. ###

TLDR: Figma delivered a strong beat-and-raise quarter with accelerating revenue growth, strong AI monetization, and improving enterprise adoption trends. Investors responded positively because AI products are driving incremental revenue instead of cannibalizing demand, although margins remain under pressure from heavy AI investment spending.

Result – Still running